In the complex world of commercial real estate management, decision-makers often face a fundamental challenge: how to effectively bridge operational data with forward-looking investment forecasts. In this article we present a framework with "Two Layers of Data", two perspectives of which require different approaches and data types. Let's explore how these distinct but complementary layers function and why understanding both is crucial for successful real estate investment management.

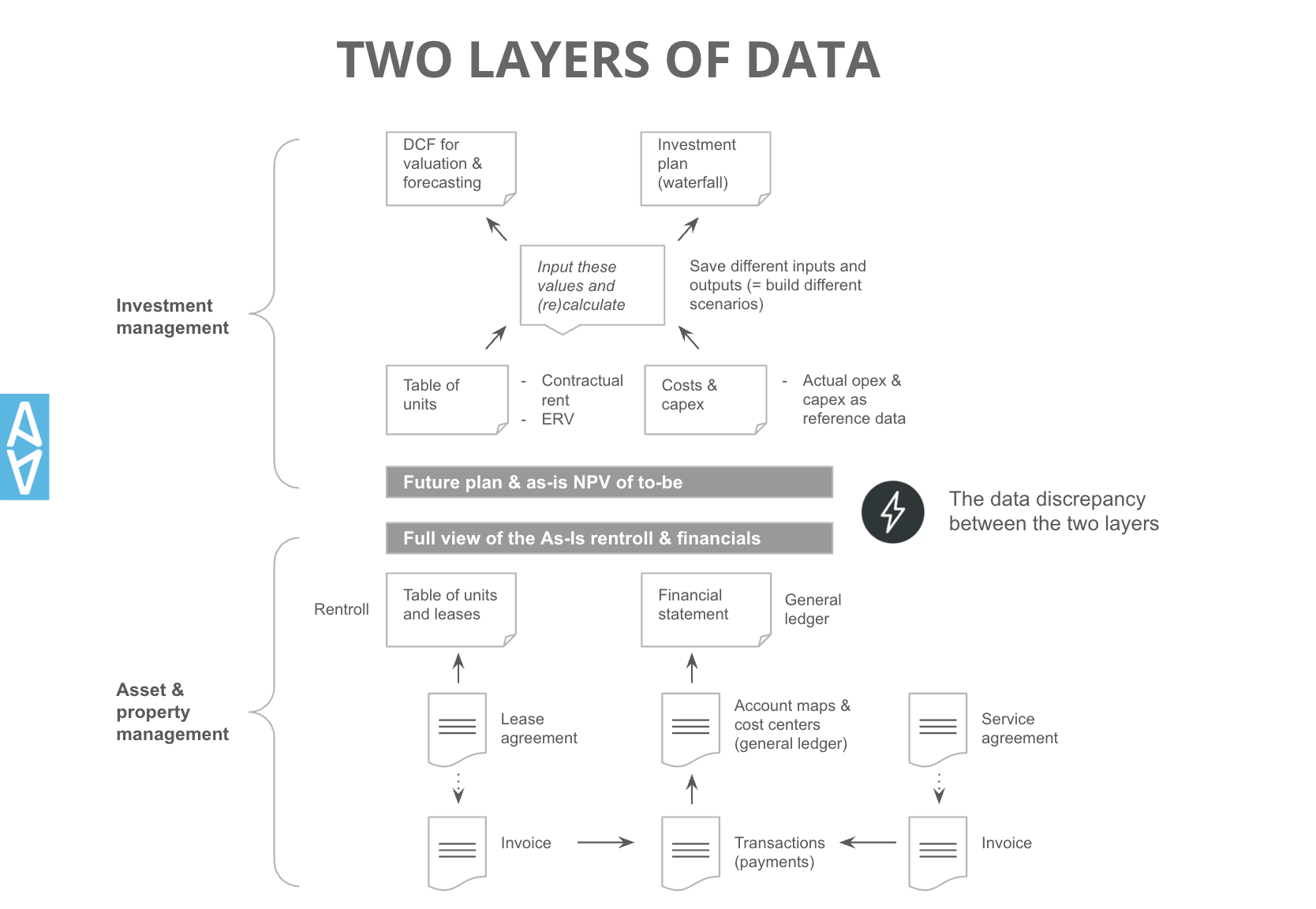

Commercial real estate operates on two primary data layers:

While these layers interact, they serve different purposes and often require different data sets. This discrepancy creates both challenges and opportunities for real estate professionals.

The foundation of any real estate operation is its accounting system. This layer captures the "as-is" financial reality and typically includes:

This data reflects historical performance and current operational status. It answers the question: "What is happening right now in our properties?" The accounting perspective is essential for compliance, tax reporting, and understanding current cash flow, but it has limitations when projecting future performance.

When valuing properties or planning investment strategies, relying solely on accounting data becomes problematic. Future-oriented analysis requires:

This layer addresses the question: "What could happen in the future with our properties?" It's fundamentally predictive rather than descriptive.

The core structural difference between these two data layers lies in their fundamental units of analysis. The accounting layer organizes information around financial accounts—general ledger codes, cost centers, and standardized financial categories. This structure excels at tracking monetary flows and maintaining compliance with financial reporting standards.

In contrast, the investment management layer organizes information around physical or contractual units — individual spaces or leases. This unit-based approach allows for granular forecasting that considers the unique characteristics of each space and its market potential.

This structural mismatch creates translation challenges. Accounting systems might track revenue by account type (base rent, service charges, parking) while investment analysis requires this data reorganized by unit (retail space A, office unit B). Converting between these structures often requires tedious mapping exercises and can introduce discrepancies when the same underlying reality is viewed through different lenses. The reconciliation between these two becomes a critical challenge for organizations seeking data-driven decision making.

As shown in the diagram, when forecasting and valuation are needed, real estate professionals typically choose between two methodologies:

This "quick and dirty" method relies heavily on assumptions and simplified modeling. Key characteristics include standardized inputs that can be quickly adjusted, high-level assumptions rather than detailed projections, and faster scenario generation. It's suitable for preliminary analysis or when time is limited, offering less precision but greater speed.

This approach might use broad metrics like "average rent per square meter" or "overall occupancy percentage" rather than unit-by-unit analysis.

This more comprehensive method incorporates rentroll-plus analysis examining each unit individually, granular assumptions about future performance, actual operational expenses as reference data, and space-by-space projections. It offers higher precision but is more time-intensive.

The detailed approach might project specific lease expirations, anticipated renewal probabilities, and unit-specific rent adjustments.

The critical connection between these layers comes in two parts: firstly, utilising the data from property & asset management layer to build the basis for the investment management, and secondly, saving different inputs for building multiple scenarios, inputting values for recalculation when assumptions change, and creating a future plan with NPV calculations.

This translation process allows investment managers to take current operational data and transform it into future projections. It's here that the art and science of real estate investment analysis merge.

The separation between operational accounting and forward-looking investment analysis isn't just an organizational preference—it's a necessity because:

To effectively manage both layers of real estate data, consider these approaches:

Successful real estate investment management requires both a clear-eyed view of current operational performance and an imaginative but disciplined approach to forecasting. By understanding the relationship between these two data layers, professionals can make more informed decisions.

The parameterized approach offers speed and flexibility for rapid scenario testing, while the detailed approach provides the precision needed for final investment decisions. Most organizations benefit from capabilities in both methodologies, applying them as appropriate to different situations.

Ultimately, the challenge isn't choosing between accounting data and investment projections—it's building systems and processes that allow these two perspectives to inform and strengthen each other.

If you are interested how Assetti could support you in making this reality, happy to connect.

.png)